By separating each value into parts, experts can improve the thought of how the profit is utilized, reinvested in the business, or kept in real money. This oversight becomes more important when analyzing a company’s health. Financial data alone can tell us how much a company owns and owes. Still, it doesn’t explain how efficiently it’s using the resources or managing operations on a day-to-day basis. Metro Corporation earned a total of $10,000 in service revenue from clients who will pay in 30 days. From setting up your organization to inviting your colleagues and accountant, you can achieve all this with Deskera Books.

Dual Aspect Concept in Accounting FAQs

Because of the two-fold effect of business transactions, the equation always stays in balance. Equity represents the portion of company assets that shareholders or partners own. In other words, the shareholders or partners own the remainder of assets once all of the liabilities are paid off. Receivables arise when a company provides a service or sells a product to someone on credit. An asset is a resource that is owned or controlled by the company to be used for future benefits. Some assets are tangible like cash while others are theoretical or intangible like goodwill or copyrights.

Owner’s Equity

By analyzing the loan cost against the potential gains from the new asset, the company can determine if the transaction positively impacts its financial health and equity in the long term. A cost-benefit analysis can further help to assess whether taking the loan is beneficial. If a company keeps accurate records using the double-entry system, the accounting equation will always be “in balance,” meaning the can i do my taxes from my iphone left side of the equation will be equal to the right side. The balance is maintained because every business transaction affects at least two of a company’s accounts. For example, when a company borrows money from a bank, the company’s assets will increase and its liabilities will increase by the same amount. When a company purchases inventory for cash, one asset will increase and one asset will decrease.

What Is The Double-Entry Bookkeeping Method?

- While the accounting equation is essential, it has limitations.

- For starters, it doesn’t provide investors or other interested third parties with an analysis of how well the business is operating.

- As you can see, we added all transactions that related to the bank to arrive at our ending balance of $20,000.

- He is the sole author of all the materials on AccountingCoach.com.

- While this approach is quite straightforward and can be verified, it does not consider the impact of inflation, depreciation, market fluctuations, and other factors.

- In our examples below, we show how a given transaction affects the accounting equation.

This then allows them to predict future profit trends and adjust business practices accordingly. Thus, the accounting equation is an essential step in determining company profitability. The fundamental accounting equation, also called the balance sheet equation, is the foundation for the double-entry bookkeeping system and the cornerstone of the entire accounting science. In the accounting equation, every transaction will have a debit and credit entry, and the total debits (left side) will equal the total credits (right side). In other words, the accounting equation will always be “in balance”.

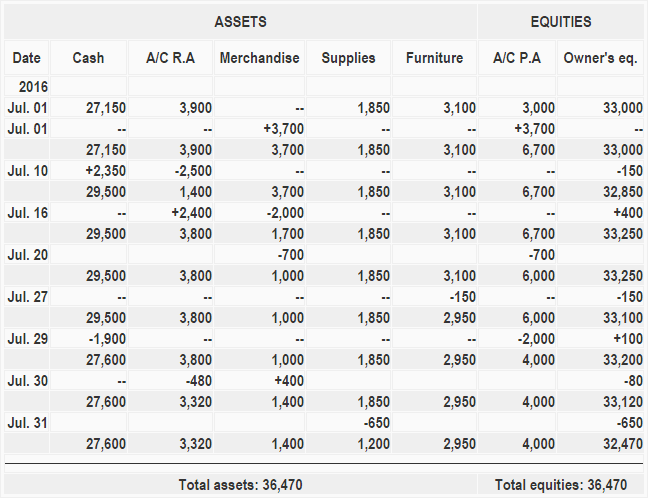

Aspects like customer satisfaction, supply chain efficiency, and innovation efforts can go missing even though they can directly impact the company’s current and future performance. So, while the accounting equation gives numerical balance, it lacks the necessary depth to make informed operational decisions. Now, these changes in the accounting equation get recorded into the business’ financial books through double-entry bookkeeping. On 5 January, Sam purchases merchandise for $20,000 on credit.

What Are the 3 Elements of the Accounting Equation?

Double-entry accounting is a system that describes and lists the business processes involved in the financial management of a company. The lenders of a business have the legal and economic rights to the assets of that business. For example, a creditor who lends money to a restaurant owner has a right, in a legal sense, to a portion of the business’ assets until the business repays its debt. The owner of the business also has an interest in the assets because they have invested in the business. If these estimates are wrong, they can have long-term consequences.

If the business uses cash to purchase an asset, the total amount of assets remains the same, but the composition changes. The owner’s equity is the value of assets that belong to the owner(s). More specifically, it’s the amount left once assets are liquidated and liabilities get paid off. An asset can be cash or something that has monetary value such as inventory, furniture, equipment etc. while liabilities are debts that need to be paid in the future. For example, if you have a house then that is an asset for you but it is also a liability because it needs to be paid off in the future. On 28 January, merchandise costing $5,500 are destroyed by fire.

The fundamental accounting equation, also known as the balance sheet equation, represents the relationship between the asset, the liability, and the equity of a company. Assets are all the properties that a company owns and on the other hand, liabilities are what the company owes. Moreover, companies may underestimate the cost of long-term debt or overestimate the value of long-term assets. This is particularly important for businesses making investment decisions or evaluating projects with cash flows spread over multiple years. Therefore, while the accounting equation is a fundamental tool, a lack of consideration for the time value of money limits its usefulness in long-term financial planning.